Trading less recessions for weaker growth

Economic recessions are less frequent than they used to be, but economic growth is also weaker... is that tradeoff worth it?

Economists and policy makers get a lot of shit for their job performance. Rightfully so, economists can be pretty bad at predicting things and economic policy often feels incoherent.

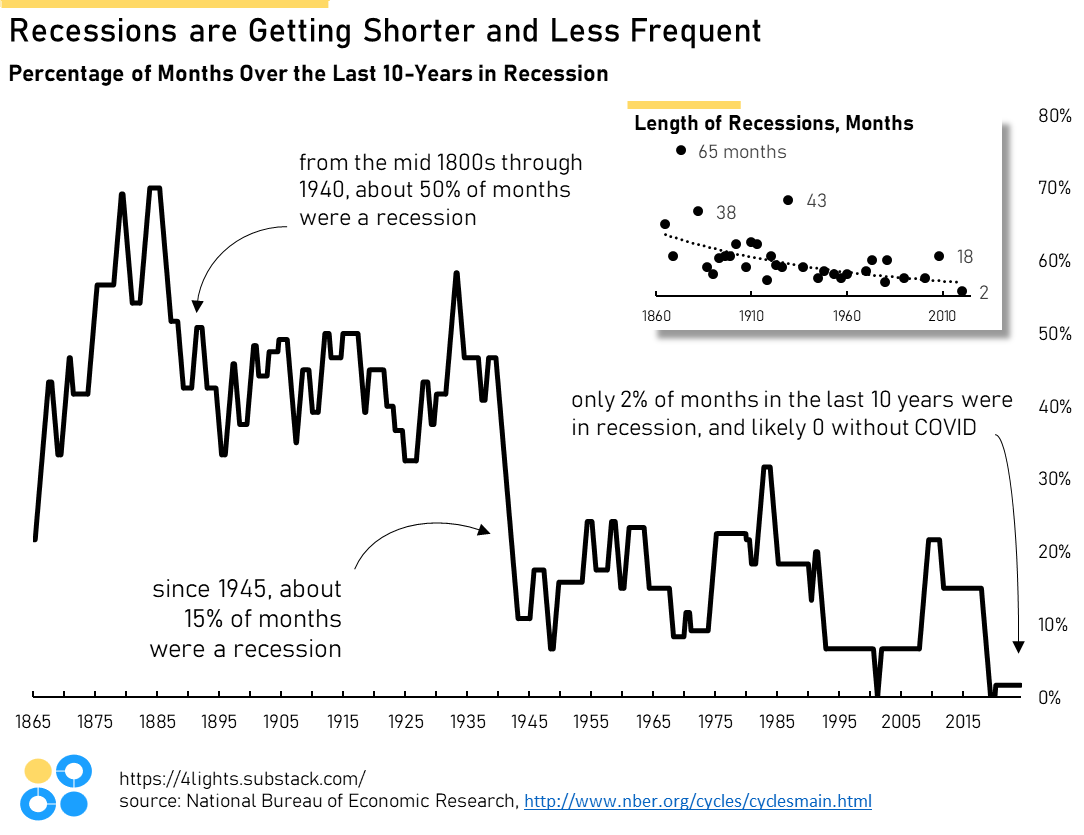

But, if we’re so bad at economics, why are we experiencing fewer and fewer recessions1 over time? In a given 10-year period in the late 1800s to early 1900s, about 50% of time was a recession. After the Great Depression and World War II, it to around 15%. Now, in the last 10 years, only 2% of months have been in a recession (and that likely would have been 0% without COVID). In addition to becoming less common, recessions are also generally getting shorter over time.

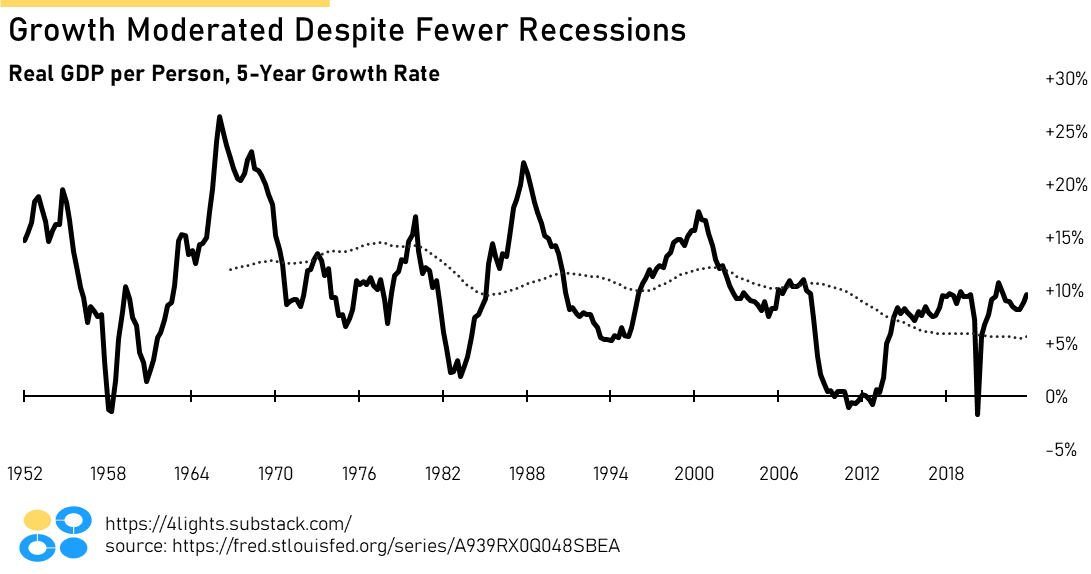

So, what’s the catch? Recessions are less frequent, but they are different. We simply aren’t bouncing back as quickly as we used to. Everyone remembers the pain of the 2007-2009 “Great Recession”, but what about the the forgotten 2001 recession? It was also an astoundingly slow labor recovery. Job losses continued for another 2 solid years after the recession officially ended, and it took another 1.5 years to get back to the previous peak employment level.

Although growth numbers have been pretty outstanding in the last couple of years, it seems unlikely we will get to a place with infrequent recessions and consistent, strong expansion. What do you think?

Recessions isn’t just a karaoke dive bar in Washington DC. The National Bureau of Economic Research defines it as a “significant decline in economic activity that is spread across the economy and that lasts more than a few months.”